Investor News

Bill shock as standard of living slumps

It will come as no surprise that high electricity prices are a major contributor to the recent slump in our standard of living.

The below article from The Australian confirms the damage:

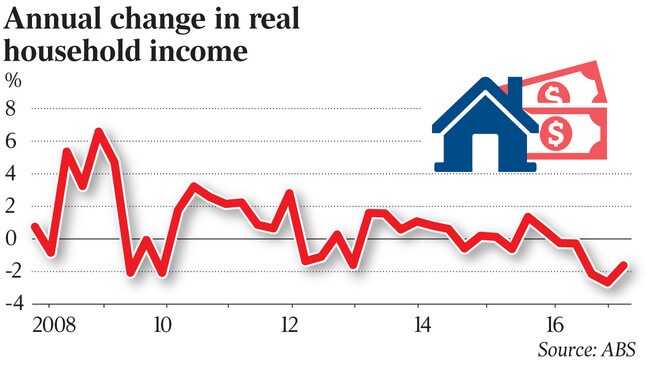

After allowing for inflation, taxes and interest costs, average household incomes dropped 1.6 per cent in the year to September, capping a sustained fall in living standards that has not been seen since the 1990-91 recession.

The underlying dynamic includes 'bracket creep' as wage rises push workers into high tax brackets, where a serious chunk of their increase is taken by the government.

The ABS Wage Price Index shows a 1.9 per cent rise last year, but this is measured before tax and records the average increase for each job. National accounts show that personal income tax collections are rising much faster than pre-tax wages, partly because more wage income is being pushed into higher tax brackets. They show a 4 per cent lift in taxes per capita over the year to September, absorbing 60 per cent of the increase in wage income per person, which rose only 1 per cent.

National Australia Bank's head of research Peter Jolly commented:

“Households are spending their money on non-discretionary items — the things you can’t avoid — and they’ve been going up much more quickly than discretionary items.”

Taking a deeper dive into electricity pricing, the Residential Electricity Price Trends Report by the Australian Energy Market Commission (AEMC) is a useful reference to understand what's happening to electricity (full report here).

In short, it identifies the four main components making up the residential electricity price:

- Network costs: comprised of transmission and distribution costs, which account for around 40 to 55 per cent of the price

- Wholesale market costs: which account for around 30 to 40 per cent of the price in most jurisdictions

- Environmental policy costs: which directly account for around 5 to 15 per cent of the price

- Residual component: which accounts for around 5 to 15 per cent of the price in most jurisdictions.

The 2017 report shows that the trends in residential electricity prices are primarily driven by wholesale electricity purchase costs in all jurisdictions.

It also highlights the impact of environmental policies such as the Large Scale Renewable Energy Target (LRET), which results in the following cycle:

- the entry of wind and solar generators, which have lower operating costs compared to coal and gas-fired generators and therefore reduce wholesale prices in the short-term

- over time, low wholesale costs mean some gas- and coal-fired generators may not recover their operating and maintenance costs, resulting in exit from the market

- to the extent the LRET contributes to generation exit, it will tighten the supply and demand balance, leading to higher wholesale prices. This cycle has contributed to the recent high wholesale prices in the NEM.

Importantly, the report highlights how the LRET scheme design contributes to spot price volatility by reducing the incentives to enter into firm hedging contracts, as generators receive a separate source of revenues from LGCs.

As wind and solar generators are able to seek recovery of their fixed costs from outside of the wholesale electricity market they do not provide firm hedging contracts. The design of the LRET scheme means revenue certainty is obtained from LGCs as well as from wholesale electricity spot prices. As traditional generators who offered the firm hedging contracts retire, under the LRET, there will be fewer generators to supply firm hedging contracts. This results in upward pressure on wholesale electricity contract prices. The South Australian forward contract market has been affected by the lack of firm hedging contracts.

The LRET scheme design incentivises investment in intermittent renewable generation that do not sell firm hedge contracts. As the output of intermittent generation depends on wind and solar conditions which vary over time and cannot be controlled, these generators are not in a position to defend firm hedge contracts. The intermittent nature of this generation is not reflected in wholesale spot prices, as these prices do not reflect the value of firm capacity (i.e. dispatchable capacity).

Further, given that fewer generators may provide contracts, the risk faced by retailers from volatile spot prices may increase due to the inability to hedge their position. This will over the longer term also potentially affect the level of retail competition.

The report does forecast a drop in residential energy prices over the next few years, which is consistent with the comments in the below article.

The price drops are expected to be driven by 5,300 MW of new generation that is committed or expected (modelled) to enter the NEM over the period 2016/17 to 2019/20, of which the majority (4,900 MW) is renewable generation.

But, here's the deal; around 20% is expected to be solar PV, which has about a 17% capacity factor. The rest is wind, which has around a 30% capacity factor.

The outcome will be an average generation of 166MW of solar and 1,176MW of wind. The problem of what to do when the sun doesn't shine and the wind doesn't blow still isn't solved and requires a further expenditure on storage or the backup of expensive gas.

In short, while the direct impact of environmental costs may be 5-15% of our electricity bill, the same environmental policy also impacts the wholesale cost component, tending toward higher pricing due to the uncertainty of supply against relatively certain (or at least reasonably predictable) demand.

Read more...

Bill Shock as standard of living slumps

David Uren | The Australian | 5 January 2018

Australians have endured their longest period of falling living standards in more than a quarter of a century as growth in costs outstripped earnings for the fifth consecutive quarter, leaving households worse off than they were six years ago.

Source ($): Bill shock as standard of living slumps