Investor News

Coal power plant may shut early... or not.

An article by Matt Chambers in ‘The Australian’ (below) highlights a confounding paradox as our leaders strive to deliver long-term reliable, affordable energy policy outcomes.

The Story…

AGL, the owner of "Loy Yang A" brown coal power station in Victoria, said that depending on ‘the market’, they may close ten years earlier than the current 2048 strategy.

AGL, under former chief executive Andy Vesey, committed to getting out of coal-fired power by 2048, which is the end of life for Loy Yang, Victoria’s and AGL’s newest coal-fired power plant, built in the 1980s.

But in a briefing to investors at the Latrobe Valley plant, AGL operations boss Doug Jackson said the company would need to make a big mid-cycle investment in the late 2020s to keep the plant going that long.

“Our target today is making 50 years, which is 2038,” Mr Jackson said. “We want to be careful we don’t just say ‘let’s go all the way to 2048’ today.”

AGL is in the middle of a $900 million spend over six years on the plant and the associated giant coal mine on its site, preparing it to run until 2038.

This includes refurbishing generators and turbines.

A similar amount will be required to be committed to next decade to get the plant running to its full potential 60-year life. “We’ve made commitments to this (2038) strategy so far,” Mr Jackson said, referring to a presentation slide that showed the company’s current plan for keeping the plant operating reliably.

“We will make future commitments to this (2048) strategy depending on the market, so we’ll keep a close watch on that.”

The quick reversal…

AGL Loy Yang general manager Steve Rieniets quickly' clarified' this the next day, saying to Jarrod Whittaker of the Latrobe Valley Express that the company was committed to its 2048 scheduled closure date.

"We had investors on-site yesterday and some of the comments made during that presentation were in the context of capital expenditure planning, but our current plans as to closure is to close no later than 2048 and our existing spending on the plant indicates that's our current plan," Mr Rieniets said.

He said the company could remain in the region beyond 2048 and pointed to the company's involvement in the Hydrogen Energy Supply Chain pilot project which aims to convert brown coal from the Loy Yang mine to hydrogen as an example of the company's broader involvement in the region.

AGL has invested about $100 million in a major outage on unit four and refurbishment of a dredger and had done so in the expectation of a long-term return, Mr Rieniets said.

It will invest a total of $900 million into the plant between 2016 and 2021.

What’s behind this reversal?

The Australian highlighted the marginal generation cost of $10 per MWh, compared to an average wholesale price of $92.33 per MWh (2018).

This begs the question, why wouldn’t AGL continue to invest to stay open through to 2048 to continue to extract such ‘healthy’ margins for its shareholders?

We suspect the mention by AGL’s Doug Jackson of ‘keeping an eye on the market’ had more to do with keeping an eye on government intervention in the market as opposed to the market itself.

What’s the state government's position?

Difficult.

In just the past 3 years, the state government has overseen a simultaneous drop in electricity affordability and reliability as wholesale power prices jumped from $30MWh (2015) to $92MWh (2018), and outages increased during periods of peak demand.

This is due to state energy policy, which has contributed to the addition of expensive wind and solar, the unplanned exit of 22% of the state's brown coal capacity, and an increased reliance on gas-fired power at a time when gas prices have doubled.

The government's solution to too much expensive intermittent wind and solar has been to subsidise more expensive intermittent wind and solar with batteries.

So, why even suggest an early closure?

It appears to rest on a paradox.

What direction could ‘the market’ (i.e. government intervention) take in 10 years that could eliminate such a huge margin advantage for Loy Yang A?

The answer appears to be ‘diversification’.

Indeed, all the big ‘gentailers’ – AGL, Energy Australia, and Origin—have been 'diversifying' their generation portfolios, adding wind, solar, and natural gas, creating conditions that may precipitate the early exit of otherwise profitable assets such as Loy Yang A.

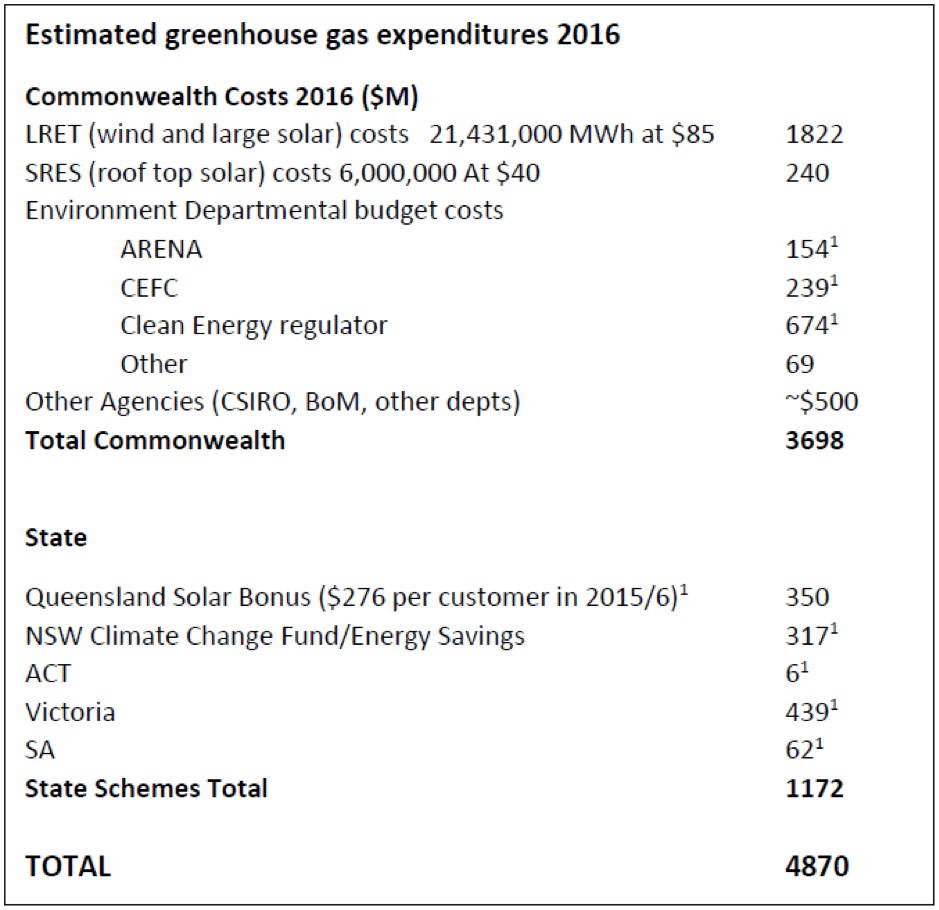

The main driver of this ‘diversification’ has not been ‘the market’ but rather government intervention in ‘the market’ via ‘subsidies’ paid from the pockets of electricity consumers and taxpayers. Nearly $5Bn a year, based on 2016 data.

The paradox of this subsidy-driven ‘diversification’ into expensive wind and solar is that energy options are increasingly constrained with the closure of coal-fired power stations and increasing electricity and gas prices.

The addition of subsidised wind and solar has reduced the demand for coal-fired power.

In the case of wind, it takes ‘first place’ in the queue on the supply side, and in the case of residential solar, it hollows out the demand side.

Wind's often sudden intermittency requires gas and hydro to fill that gap, driving up gas demand and price in a constrained gas market.

The push to encourage and, indeed, mandate wind and solar uptake also has cost implications for the network, as intermittency and changes in distribution require upgrades to maintain stability.

The result is the current paradox. An unintended consequence.

Gentailers who own wind, gas and brown coal power assets unintentionally benefit from energy policy subsidies in two ways.

Firstly, by guaranteeing a return on the investment in otherwise uncommercial wind power via the mandated purchase of their output ahead of coal, and secondly, through reduced reliability of the network, driving up spot prices and increasing the margin received by coal and gas power stations.

Energy policy development needs to factor in these distortions if there’s any chance of restoring reliability and affordability.

One solution currently being deployed globally to deliver reliable and affordable power is high-efficiency, low-emissions (HELE) coal technology. Japan plans to build 45 such HELE plants, and Egypt has recently given the green light to build the world’s largest HELE power station.

The problem for Victoria is its wet brown coal isn’t suitable for use with HELE power stations.

It needs to be efficiently and cost-effectively dried first.

Our Coldry process is the solution, capable of drying Victoria’s brown coal for use as a ‘gateway’ to lower emission, higher efficiency, and higher-value applications.

Through the deployment of an efficient and cost-effective drying technology via Coldry we can transition away from the current model of ‘gentailer’ dominated brown coal ownership and narrow, low-value use, toward an innovation-driven model that enables new industries such as fertiliser production, gas, hydrogen and solid fuel for industrial energy applications.

By promoting brown coal technology and application diversification, our government can incentivise technologies that break the dominance of the ‘gentailers’ current model. While this may not solve the paradox of the cheapest form of power generation being forced out by more expensive wind and solar, it can provide a solution that promotes a better, lower emissions future for brown coal.

Read more...

AGL’s Loy Yang A brown coal power station may close early

The Australian | 23 October 2018 | Matt Chambers

AGL Energy could close the big Loy Yang A brown coal power station in Victoria — the east coasts lowest-cost baseload generator — 10 years earlier than its stated 2048 end of life if power markets next decade dont justify big expenditure on the plant to keep it going.

Source: Coal power plant may shut early