Investor News

High gas prices here to stay

The recent and rapid hike in electricity prices here in Australia is caused by several factors.

Network gold-plating and intermittent Wind and solar shoulder significant blame. But we also have a gas-price problem, as highlighted in the below article by Matt Chambers in The Australian ($).

Gas and pipeline chiefs say the higher prices are here to stay and that Australian industry must find a way to adapt to the rapid doubling or tripling of gas prices after the opening of the east coast to LNG exports in the past few years and rising onshore development costs.

Before diving into the gas-price issue, it may help to revisit the role that Wind and Solar play to understand how they're connected.

Rooftop solar power contribution to the grid is relatively predictable compared to Wind, following a bell curve that will vary in output by two main factors; seasonal variation and local cloud cover.

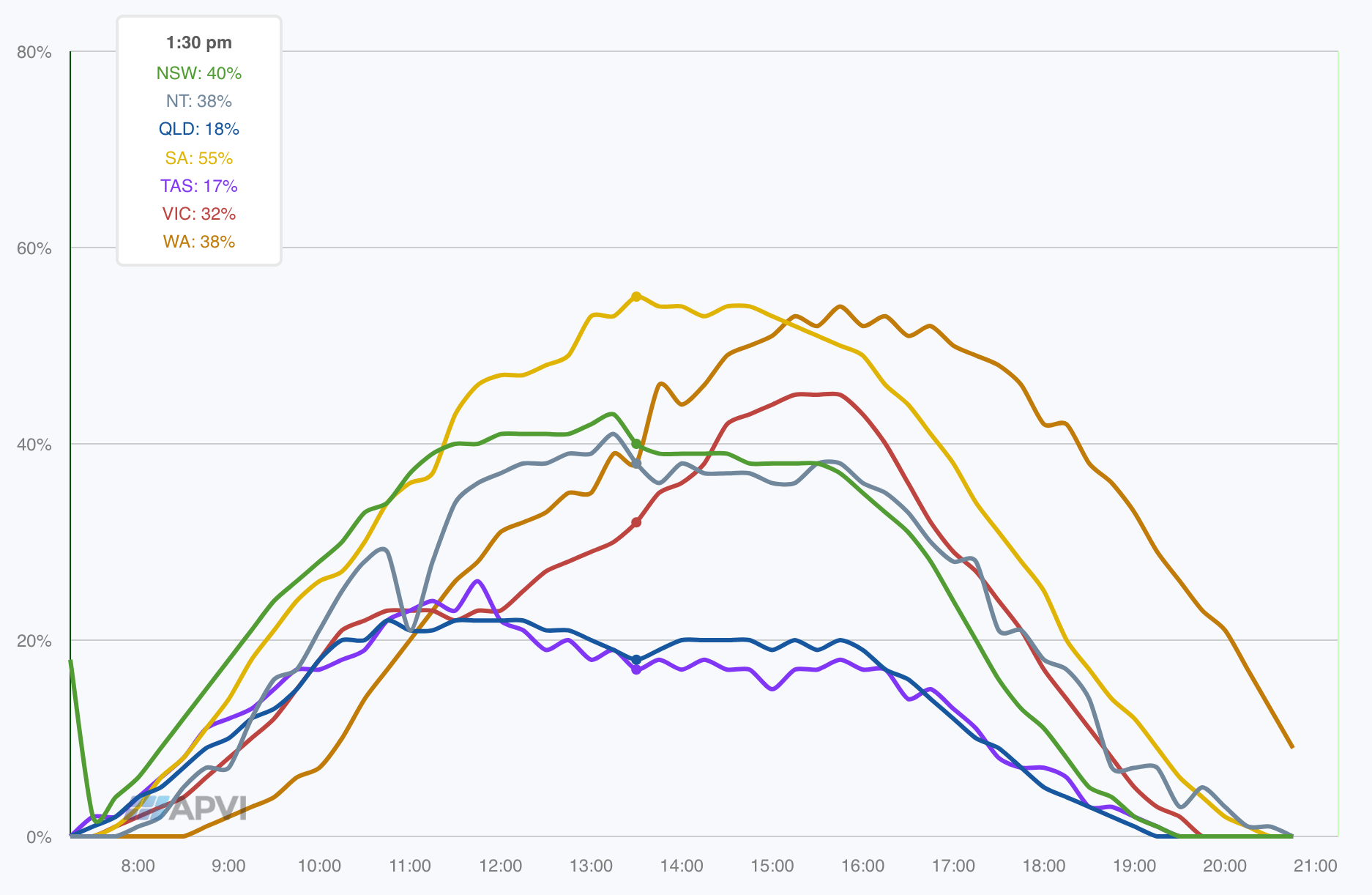

It looks like this:

The above chart shows solar PV output as a percentage of capacity.

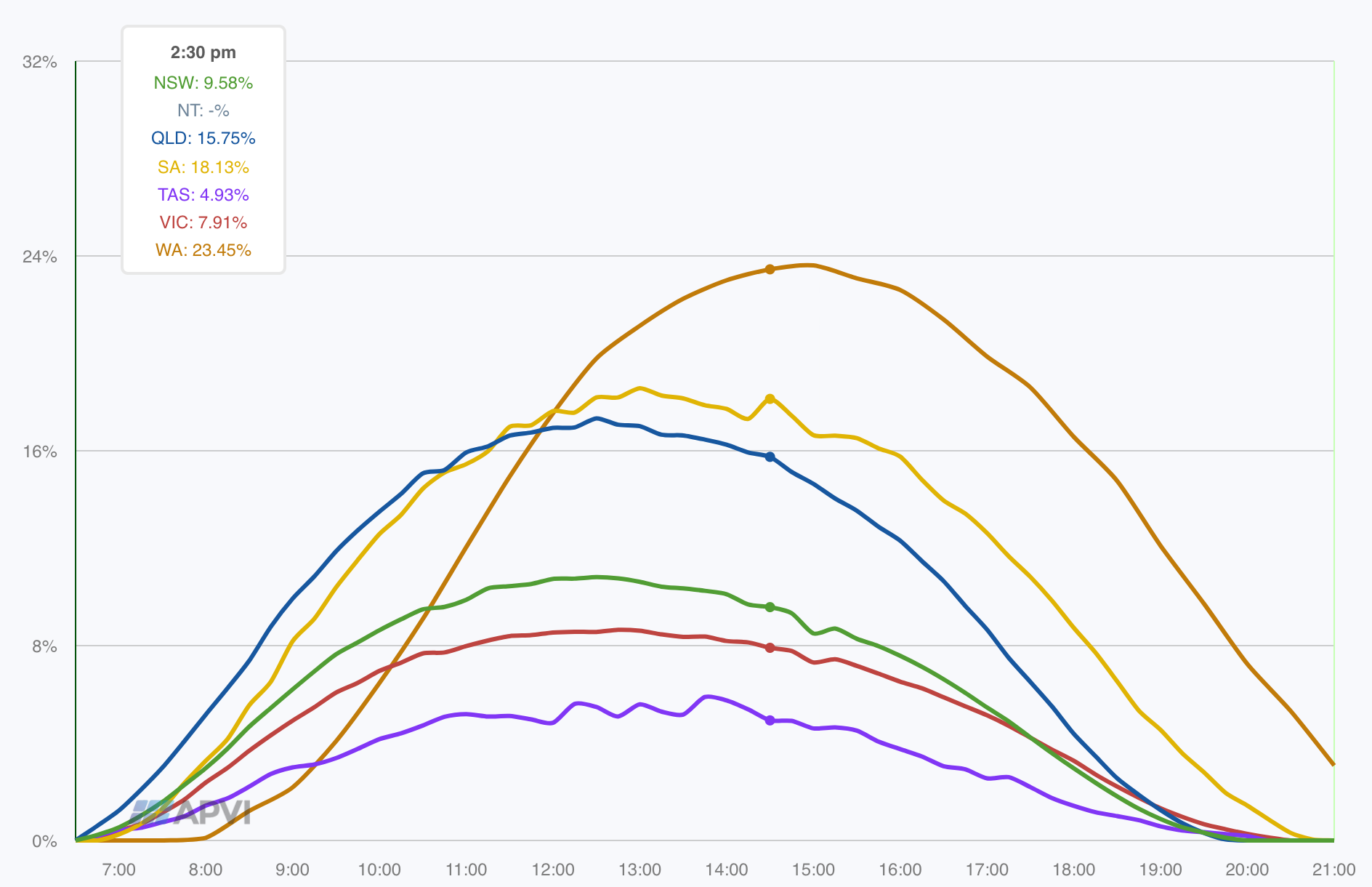

The next chart shows the estimated percentage of electricity demand being met by solar PV in each state.

The benefit of solar is that the output is less volatile across the day, making it easier for the network operator to manage supply and demand dynamics.

The problem with solar PV is that it's still expensive, requiring significant ongoing subsidies to attract uptake.

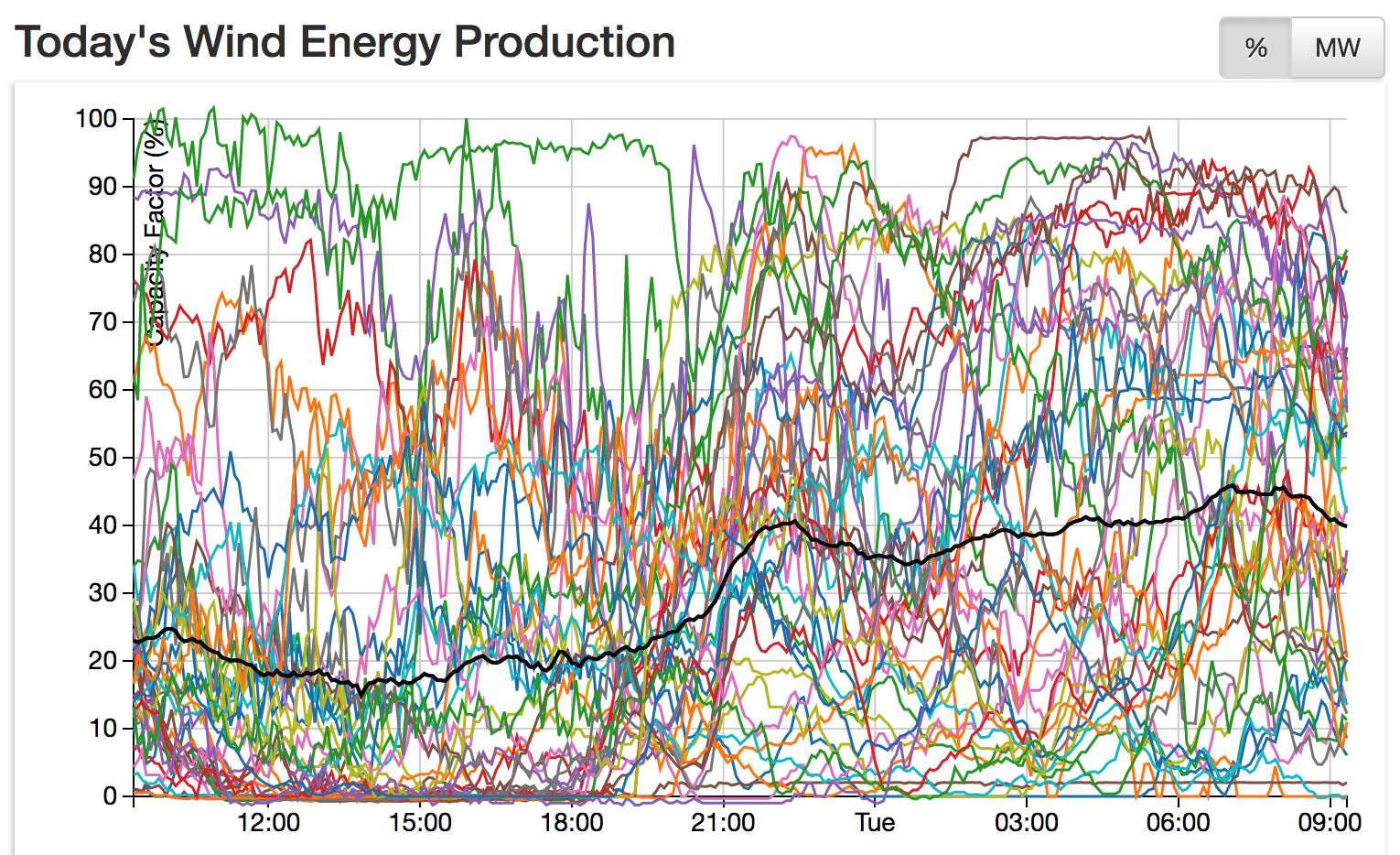

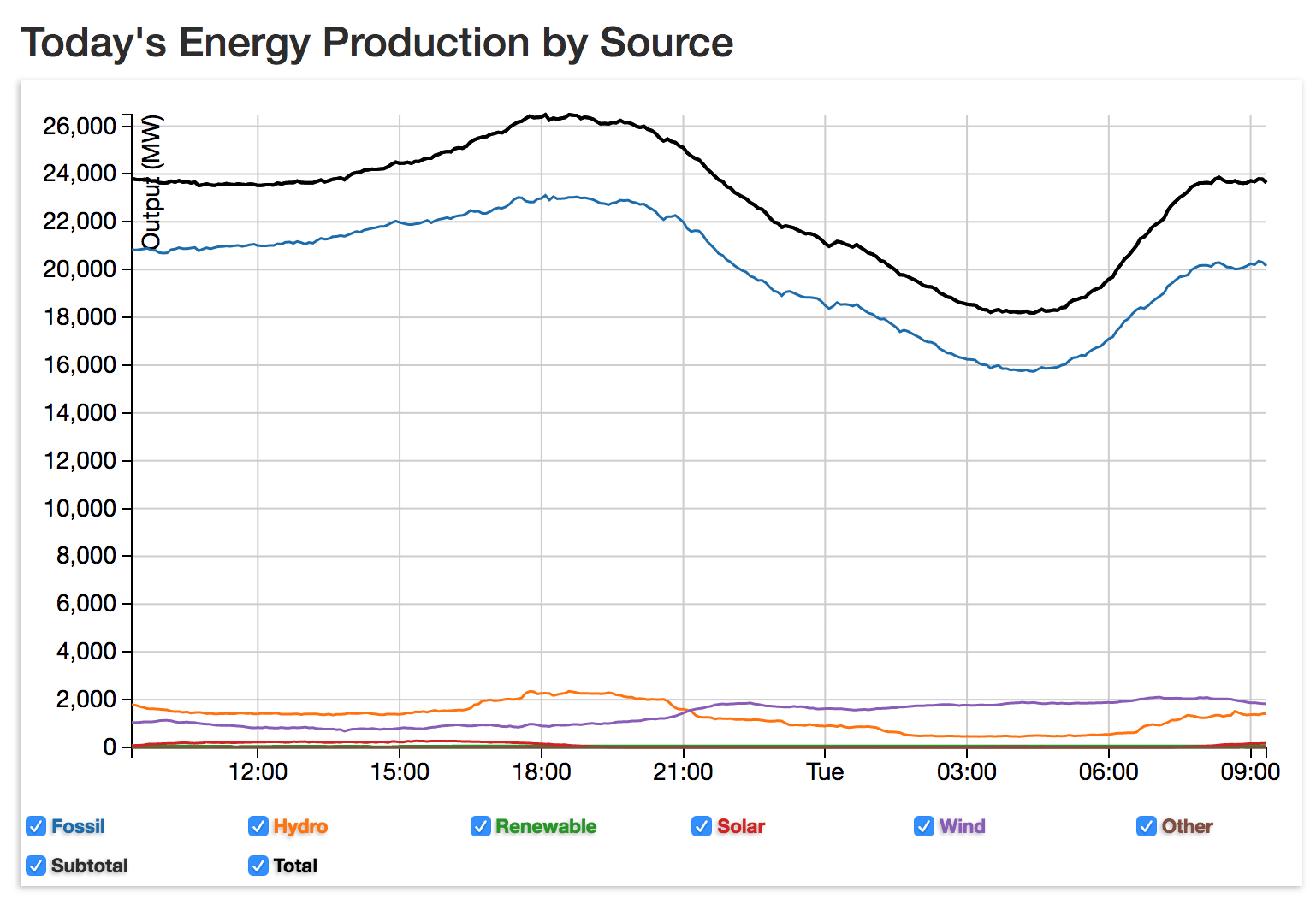

Contrast this with Wind generation, which can vary significantly over short periods, making it hard to manage:

The above chart shows the past 24 hours. The total, represented by the black line, highlights the problem often experienced with Wind... its refusal to generate in line with actual demand.

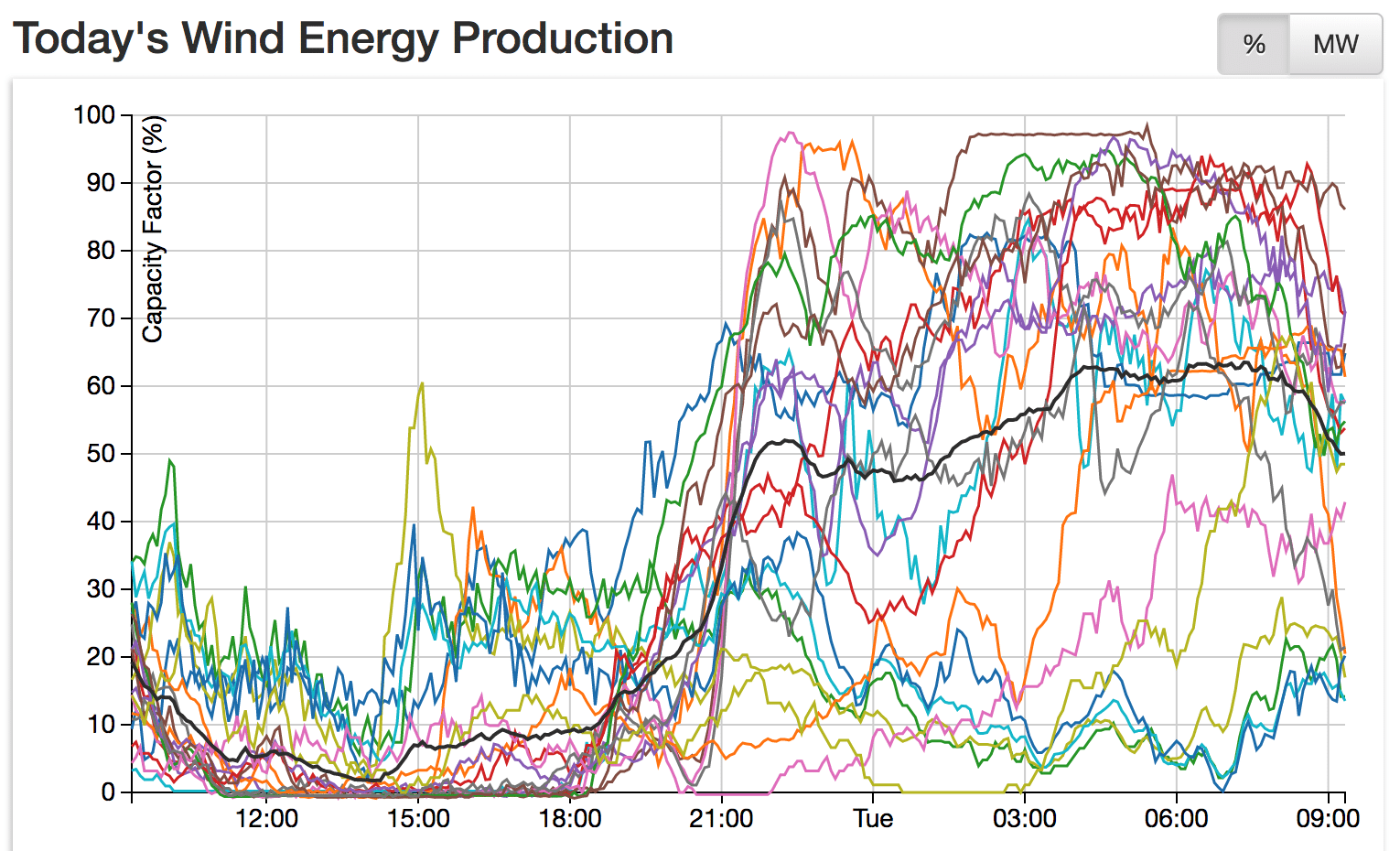

Drilling down to South Australia's data (the state with the highest reliance on Wind), we see the following performance over the past 24 hours:

SA's Windpower contribution dropped below 10% (with a brief dip below 5%) during increasing demand yesterday, picking back up overnight when least needed.

For context, hydro and natural gas filled the gaps in reliability, with coal from NSW, Qld and Victoria providing steady baseload.

Notice how solar (red line) barely registers on the above chart and how hydro (orange line) moves inversely with Wind (purple line) to help fill the gap.

With all this in mind, let's turn back to our gas-price problem.

What isn't evident in the above is the variation in gas power. It's lumped together with brown and black coal under the heading 'fossil'.

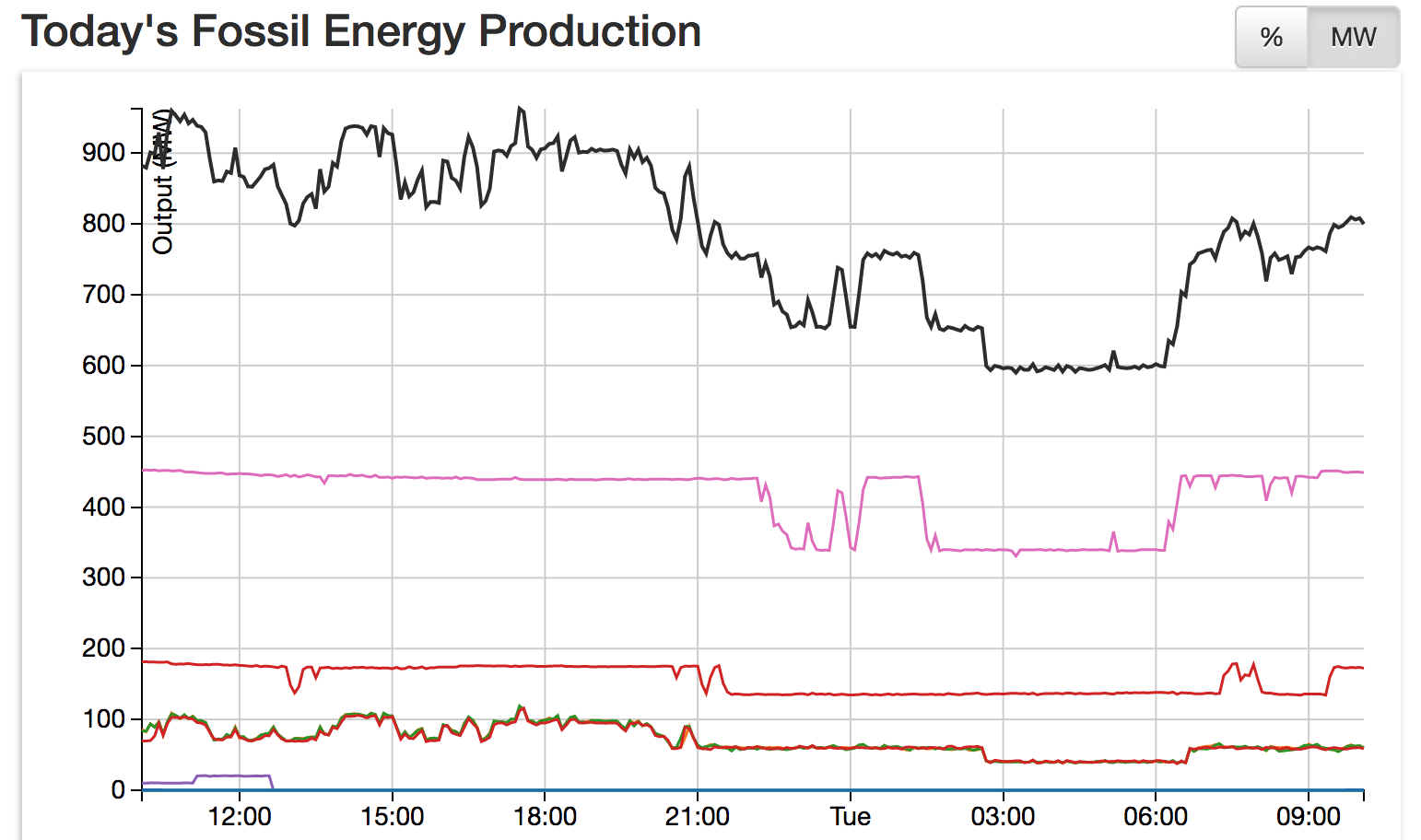

The website (www.anero.id) does allow you to drill down to specific fossil generators. SA's gas-fired profile looked like this:

In summary, since the closure of coal-fired power stations in South Australia and Victoria, there's been an increased reliance on gas to provide baseload power. Previously, gas was mainly used to cover peak demand.

This increased reliance on gas to fill the baseload gap left by the exit of coal power and its ongoing role to respond to intermittent Wind generation has come at a time when gas prices have skyrocketed from $3-$4 per gigajoule to $8-$12, as noted in the below article:

In 2017, average Sydney spot prices jumped 44 per cent to $9.20 a gigajoule, while in Melbourne, prices were up 38 per cent to $8.70, the analysis by The Australian shows.

Last month, a time of high seasonal demand, Sydney prices averaged a record $9.48 (up 6 per cent from January 2016) and Melbourne prices averaged a record $8.70 (up 3 per cent), as heatwaves hit both cities.

For energy-intensive businesses, it's a compounded problem. Many switched from briquettes to gas following the closure of the Morwell briquette plant in 2014. Gas prices have since doubled or tripled, as have wholesale electricity costs, threatening their viability.

Unfortunately, Wind and Solar PV can't deliver reliable, affordable power, and they can't service businesses that require large volumes of process heat on demand.

This has created an opportunity for ECT.

As mentioned in previous announcements, we're actively promoting our Coldry solid fuel as an alternative to gas in the Victorian and Tasmanian markets.

Our Coldry pilot plant, located 50km northwest of Melbourne, was never intended to serve commercial markets. It's not a commercial-scale facility, which means it costs more per tonne to make and couldn't compete in the global thermal coal market. However, the new norm of high gas prices means that Coldry made in our pilot plant is better value than gas for businesses that need to generate process heat.

This has attracted increasing interest and led to a series of trials with potential customers. It's also led us to explore the feasibility of a larger commercial demonstration Coldry plant here in Victoria.

At present, we have a capacity of around 15,000 tonnes a year. With further upgrades to the pilot plant, we could increase the output to 35,000 tonnes.

To this end, we're aiming to generate sufficient sales of test product from our Coldry pilot plant to establish a firm consumer base and a sound business case for proceeding with the 170,000-tonne capacity Coldry demonstration plant.

Such a plant could service those businesses currently suffering from increased electricity and gas prices and potentially enable a new generation of applications for Victoria's world-call brown coal resource, such as coal to hydrogen.

Read more below...

Energy chiefs tip more gas pain

The Australian | 26 February 2018 | Matt Chambers

Malcolm Turnbull’s gas export restriction threats have been unable to counter the impact of rising oil and Asian gas prices, with average Sydney and Melbourne wholesale spot prices jumping 40 per cent last year and January’s prices in both cities the highest on record for that month.

Source: Energy chiefs tip more gas pain