Investor News

Indian iron ore price surges

Indian iron ore prices have surged, with NMDC increasing their price for premium lump ore and fines by 39% and 8%, respectively.

Smaller merchant miners have, according to the below article in 'The New Indian Express', 'jacked up' prices by as much as 59% in some instances.

Driving the price rise appears to be a combination of increased demand, resulting from ongoing and expanded infrastructure initiatives, and supply constraints, following the withdrawal of 20 million tonnes of output due to unpaid fines by companies guilty of 'excess mining'.

This is great news for our Matmor technology.

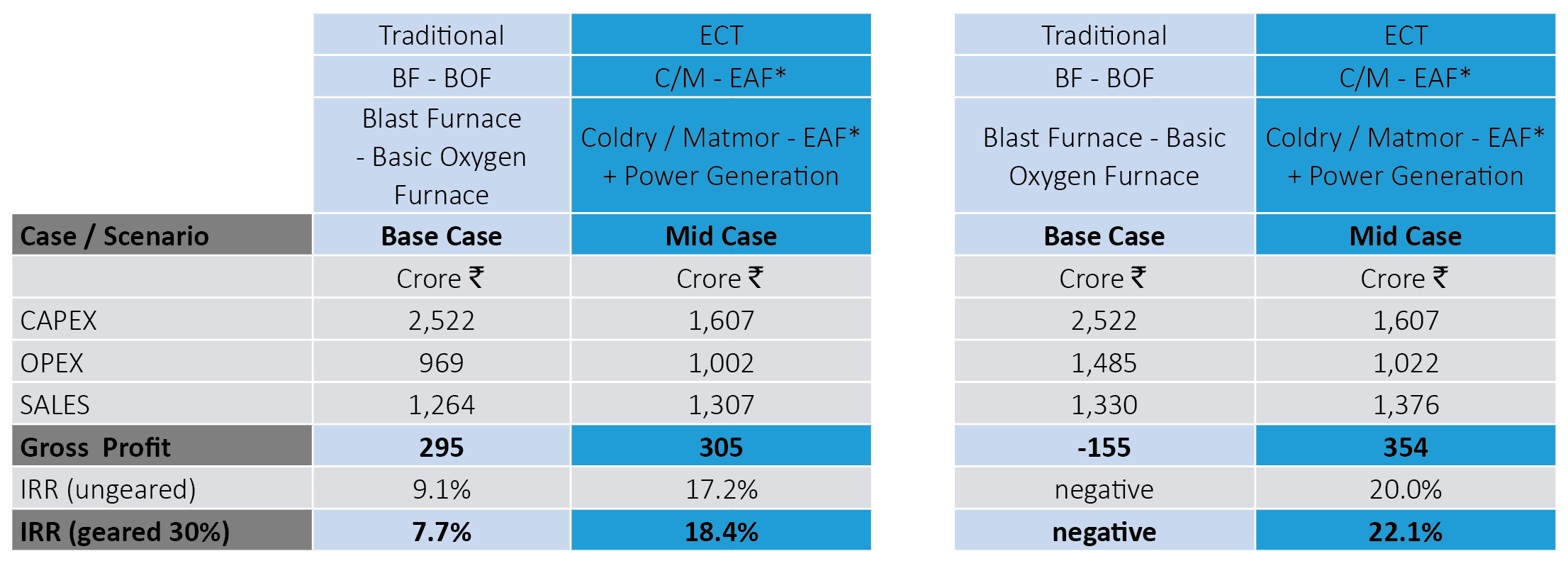

Based on the Techno-economic Feasibility (TEF) study (link) we conducted with NLC and NMDC for Matmor back in 2016, we were able to confirm the potential competitive advantage versus the 'king' of primary iron production; the blast furnace.

In our 2017 Annual Report, we updated the key benefit table; Benefit vs Blast Furnace, as follows:

Decoupling from traditional raw materials strengthens a business’ resistance to inherent price volatility:

- Critical Raw material prices have moved between early and late 2016; mainly Coking coal

- Compared below is FY16 average (left) vs. mid-October Spot (right)

Notes:

- EAF - Electric Arc Furnace

- Crore Rs. - The above table is based on the Techno-economic Feasibility Study prepared for the commercial-scale project in India. Crore is 10 million and Rs. is the abbreviation for India’s currency, the Rupee.

Matmor uses iron ore fines instead of premium grade lump ore. And it side-steps expensive metallurgical coal and PCI coal, thanks to its ability to use affordable, abundant brown coal.

The economic analysis confirmed the potential huge advantage using relatively inexpensive ingredients can have on investment return.

As ore or met-coal prices increase, the Matmor advantage gets even better.

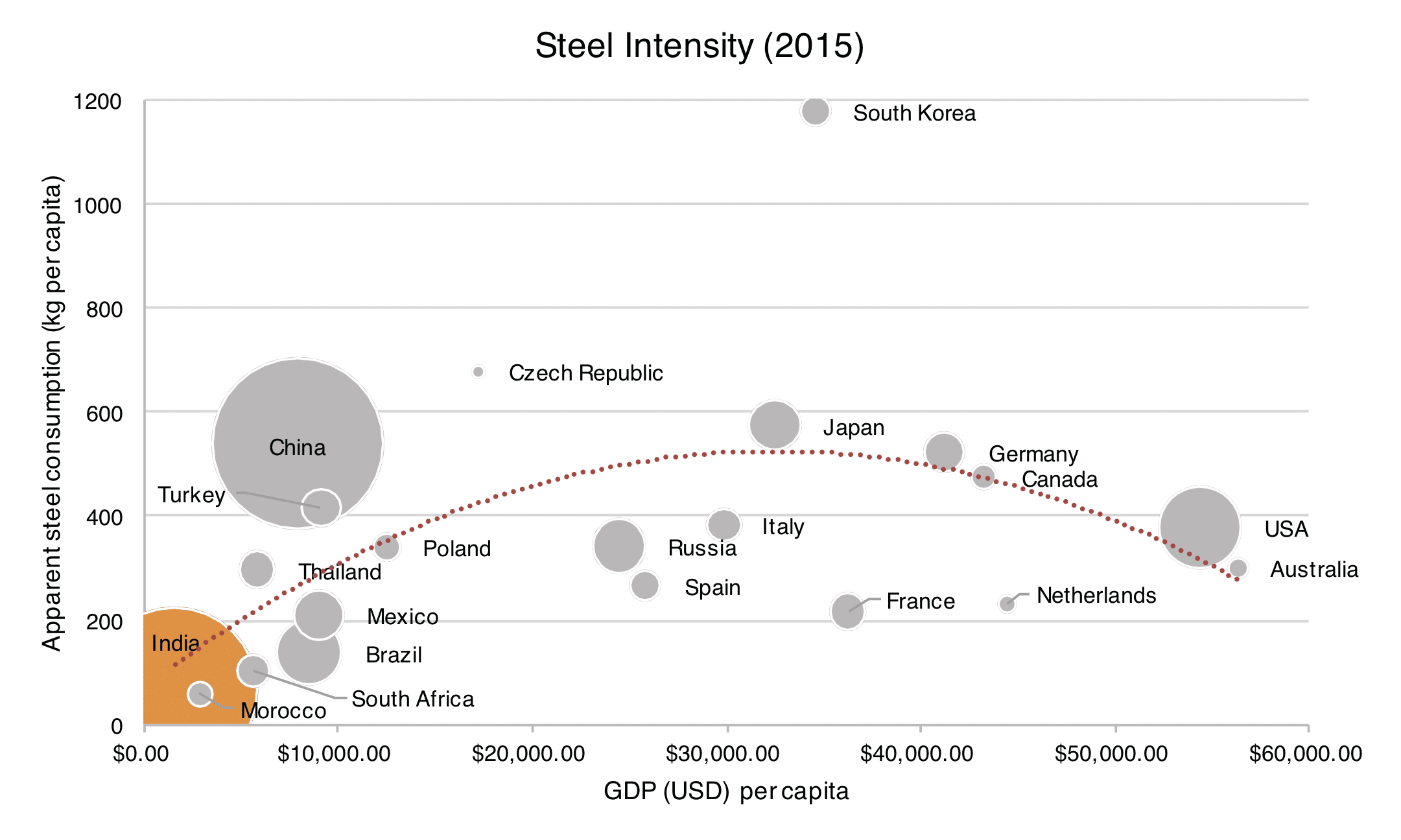

India is the place to be thanks to its major growth phase:

- Infrastructure development requiring substantial increases in iron & steel production

- Domestic coking coal reserves (effectively zero) making India heavily reliant on imports

- Low-value resources (low-rank coal & iron ore fines & slimes) able to play a major role in bridging this gap via application of ECT technologies

- World Steel Association projects India’s steel consumption growth rate to remain the highest in the world at 7.3% p.a. for 2016

- India is currently the world's third-largest producer of crude steel

- If India increase consumption to half of global average, this represents an increase of 85% or ~70Mt pa

- If Matmor can service just 5% of the growth, this represents 3.5M tpa.

The 'steel intensity' chart below illustrates this point perfectly.

To meet the Government’s ambitions, more than 200 million tonnes per annum (mtpa) capacity growth is required over the coming decades, which – with current technologies – would require the import of significant quantities of high-quality reductant (coking coal) and other materials.

Through the application of ECT’s Coldry and Matmor technology, significant capital cost savings for capacity addition is possible. Further, significant savings on the importation of high-cost, overseas sourced coking coals could be avoided, supporting the growth momentum within India’s economy.

Read more on the 'panic' below...

Panic in steel sector as ore prices soar

Bijoy Pradhan | Express News Service | 11th January 2018

BHUBANESWAR: Even as the State Government is confident of achieving iron ore production of more than 100 million tonnes in the current fiscal, in line with its target, the closure of seven major mines for failure to pay penalty for excess mining has pressed a panic button in the steel industry.

The shut down of the seven mines by State Government will bring down iron ore production by about 20 million tonne per annum...